Dubai residential market report Q1 2026: A more selective market takes shape

Dubai’s residential property market entered a more selective phase in Q1 2026, with buyers, investors and tenants becoming more deliberate in how they assess value, pricing and long-term potential.

According to the betterhomes Q1 2026 Dubai residential market report, transaction volumes remained ahead of last year while total market value continued to rise. The result is not a weaker market, but a more disciplined one, where activity is increasingly shaped by quality, location and pricing.

Dubai residential transactions reached AED 139.2 billion in Q1 2026

Dubai recorded 44,493 residential transactions in Q1 2026, up 4% year-on-year but down 17% quarter-on-quarter. Total transaction value reached AED 139.2 billion, rising 21% year-on-year, while declining just 3% quarter-on-quarter, a sign that value held up even as volumes moderated.

This gap between transaction volume and value reflects a clear shift in market behaviour. Buyers are still active, but capital is becoming more concentrated around higher-value assets and better-positioned opportunities.

The quarterly moderation was partly shaped by regional geopolitical developments in March, as well as seasonal factors including Ramadan, Eid Al-Fitr and school holidays. Rather than signalling a withdrawal from the market, the data points to delayed decision-making and a more considered approach, with March marking the clearest inflection point of the quarter.

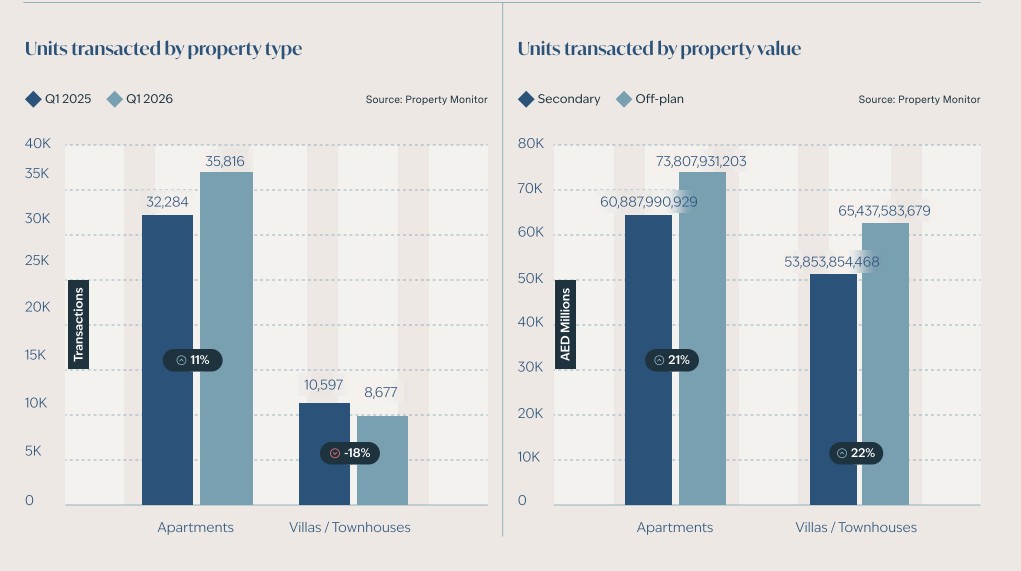

Off-plan property continues to lead Dubai market activity

Off-plan remained the strongest driver of Dubai’s residential market in Q1, accounting for 68% of total transactions.

Off-plan transactions rose 20% year-on-year, while off-plan transaction value increased 35%. This reflects continued confidence in new developments, structured payment plans and long-term capital growth opportunities.

The secondary market became more measured, with transactions declining 19% year-on-year. Buyers are becoming more price-sensitive in the ready market, where negotiation, realistic pricing and property quality are playing a larger role.

Buyer demand is shifting towards larger homes

Buyer enquiries declined 18% year-on-year in Q1, but the decline does not suggest demand has disappeared, it has become more selective.

Apartment enquiries fell 31%, while enquiries for villas and townhouses increased 15%, pointing to continued appetite for space, quality and long-term value. March marked the sharpest point of adjustment, with overall enquiries falling 33% month-on-month and 50% year-on-year, shaped by a combination of seasonal factors and regional geopolitical developments.

Apartments for sale continue to dominate overall transaction volumes, particularly through off-plan activity, but villas and townhouses for sale have remained more resilient, supply is comparatively limited and demand for larger homes remains structurally strong.

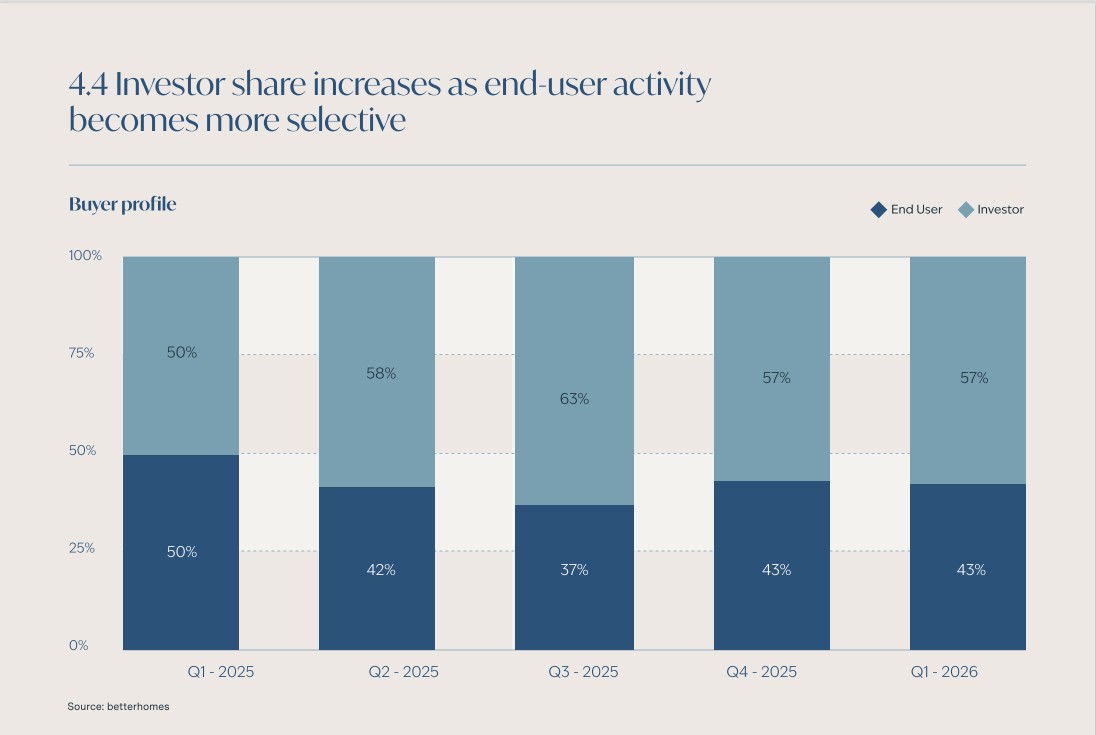

Investors remain central to Dubai real estate activity

Investor activity strengthened in Q1 2026, accounting for 57% of transactions, up from 50% in Q1 2025.

Mortgage-backed purchases represented 50% of activity, down from 58% a year earlier. Towards the end of the quarter, more buyers began using financing strategically, not because of affordability pressure, but to preserve liquidity and flexibility during a period of increased uncertainty.

This points to a more sophisticated buyer profile. Investors are still deploying capital, but with greater discipline, balancing leverage, cash position and long-term asset performance.

Dubai’s prime residential market continues to outperform

Dubai’s luxury property market remained one of the strongest areas of performance in Q1.

Transactions above AED 15 million increased 43% year-on-year to 1,214 deals, while off-plan prime transactions rose 84%. On a quarterly basis, secondary prime transactions increased 41% quarter-on-quarter, indicating short-term momentum within the established luxury segment alongside the longer-term structural growth in off-plan.

Demand in the prime segment continues to be supported by high-quality projects, global buyer interest and Dubai’s position as a long-term residential and investment destination.

Dubai’s rental market becomes more competitive

The leasing market told a more complex story in Q1. Enquiries rose 7% year-on-year, indicating stable underlying tenant demand, but leasing transactions declined 5% year-on-year and 26% quarter-on-quarter as increased supply and more selective tenant behaviour slowed deal conversion.

At a pricing level, new-let apartment prices across prime communities have come under pressure, declining between 10% and 20% year-on-year, while renewals remain largely anchored by the index. This has created a widening gap between what existing tenants are paying and what new tenants are negotiating, with tenants taking advantage of greater choice and negotiating more actively.

March saw the sharpest adjustment, with leasing enquiries falling over 40% month-on-month, shaped by seasonal factors including school holidays and Eid, alongside regional geopolitical developments. With further supply still entering the market through the rest of 2026, the coming months will indicate whether new-let pricing finds its floor or whether the gap with renewals widens further.

For landlords, this means market momentum alone is no longer enough. Well-presented, accurately priced properties continue to lease efficiently. Overpriced or poorly positioned units are seeing extended vacancy periods.

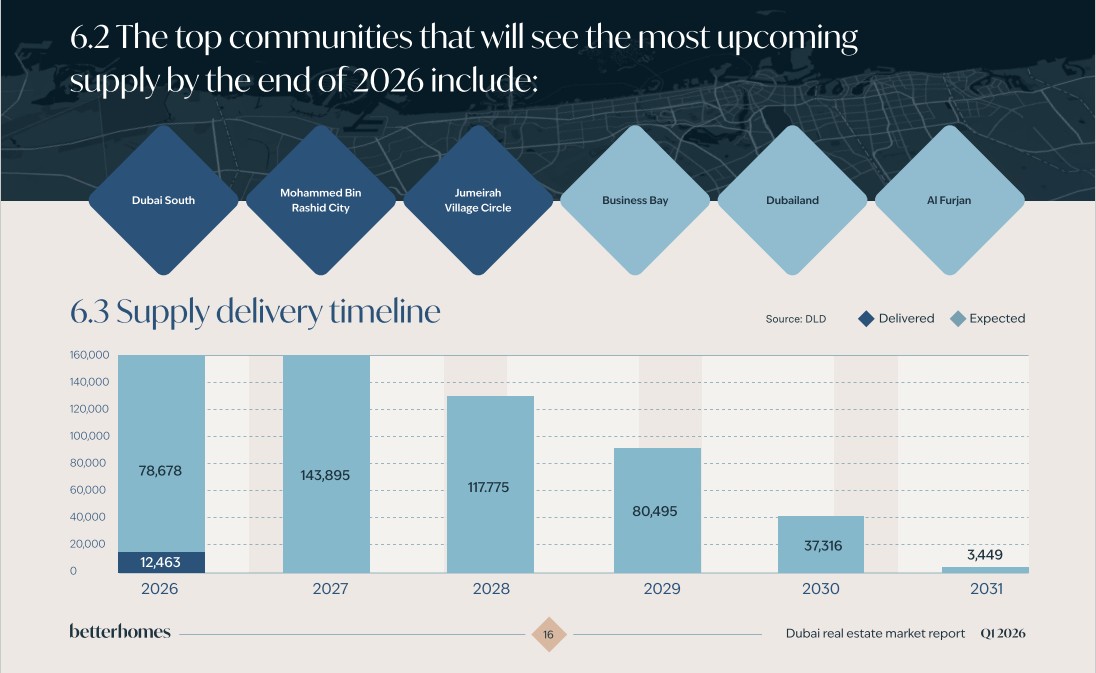

Supply pipeline: what’s coming to market

Dubai delivered 12,463 residential units in Q1 2026, with a further 78,678 units scheduled for completion during the rest of the year. Upcoming off-plan projects supply remains heavily concentrated in the apartment segment, which continues to account for the majority of planned deliveries across both sales and leasing.

In contrast, villa and townhouse supply remains comparatively limited, continuing to support resilience in these segments. Despite broader regional and seasonal factors influencing activity in Q1, developer pipelines remain on track.

As new inventory enters the market, the emphasis on pricing accuracy, product quality and strong positioning will only increase.

What this means for buyers, sellers, landlords and investors

For buyers: a more selective market creates more room to assess value carefully. Strong opportunities remain, particularly where pricing, location and long-term fundamentals are aligned.

For sellers: success will depend on realistic pricing and strong presentation. The market is still active, but buyers are less likely to chase overambitious asking prices.

For landlords: increased supply means tenants have more choice. Pricing accuracy, property condition and flexibility on terms will be key to securing stronger leasing outcomes.

For investors: Dubai remains active and liquid, but capital is being deployed with greater precision. The strongest opportunities are likely to sit in well-positioned assets with clear demand drivers, credible developers and long-term value potential.

Dubai property market outlook for 2026

Q1 2026 marks a transition from broad market momentum to more selective growth.

The market is not weakening. It is maturing.

Activity is becoming more deliberate, buyers are more value-conscious, and performance is increasingly linked to asset quality, location and pricing discipline. As supply continues to enter the market through the rest of 2026, the difference between well-positioned and poorly positioned properties will become more visible.

For anyone looking to buy, sell, lease or invest in Dubai property, the message is clear: decisions need to be guided by real data, not noise.

Get the complete betterhomes for deeper insights into sales transactions, off-plan performance, buyer demand, prime market activity, supply trends and Dubai’s rental market.